EN guest editor Phil Soar says the exhibitions industry has weathered recessions and pandemics very successfully in the past, and the latest hurdle could throw up marvellous opportunities for new and smaller companies to grow fast.

Well, are we in a recession? Arguably not, because GDP is still rising from the very low base of Covid-19 – but the markets are building in a 90% chance of one, and if it walks like a duck and quacks like a duck – it probably is a duck.

So let’s work our way through a range of anecdotes and one-liners. Average heating bills going up by £1,000 a year (that’s 3% of average income and 8% of average disposable income). Personal tax rates rising this year to their highest level in 50 years. The Brexit factor continuing to have a damning effect on trade at all levels (still 20% below where we were with Europe in 2016).

The depressive effect of a Cabinet which must have the lowest collective IQ of any since the 19th century.

High Street sales fell by 1.4% in March, while non-store retail – like Amazon – fell by nearly 8%. Train occupancy is still 70% of 2019, tube occupancy 75%. The City of London is ghost town for much of the week, and real office occupancy is no more than 50%. Government debt is at the highest level it has ever been in peacetime. The significance of the debt is that the government has to spend more in interest to service it, so must spend less than it would wish on the likes of the NHS and de-fence to stop debt going higher.

Think inflation on house mortgages and petrol prices

We haven’t even talked about what will happen when interest rates rise to keep pace with inflation and the monthly cost of refinancing a five-year mortgage doubles.

Oxford Street retailers say that they are still seeing 25% fewer shoppers than pre-Covid – and if you fancy getting away, try the queues on the M20, or the cancelled flights at Heathrow, or even P&O Ferries. And if you want to drive, enjoy petrol prices which are at their highest level ever. Latest figures this week show that the average pension will lose £7,000 in value this year because of a lack of inflation proofing.

Covid hasn’t gone away – 5% of us have it on any particular day. The economic effects of Ukraine are unknowable – the effect on food prices worldwide is already being seen and we haven’t even mentioned inflation predicted to rise to 9% or more. For many of these anecdotes, read Martin Vander Weyer in The Spectator – a marvellous economics column.

It’s being so cheerful keeps me going.

So how might all of this affect exhibitions?

None of these items induces a recession on its own – but the combination and many more points in the direction of an economic downturn which is likely to last at least two years – most recessions do.

So how might we expect it to affect our own industry? Two obvious points to begin with:

One, the UK represents less than half the turnover of all our larger companies – not that this is much of a consolation to everyone working in the UK.

Two, because we have had no comparable figures since 2019, making like-for-like interpretations is as complex as it has ever been. Having said that, there is no reason why 2019 should not be a baseline for our thinking.

In past recessions visitors fell 20% and square metres 15%

So what happened in previous recessions – as far as we can tell?

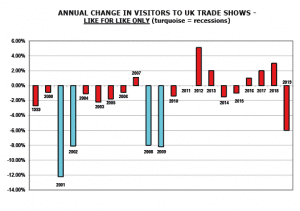

There have been three clear recessions in the three decades for which we have some information – 1990-92, 2000-02, and 2009-2011.

The chart (pictured) shows what happened to visitor numbers at trade shows in the last two. This is like-for-like year-on-year, so includes only shows for which data is available in consecutive years, and does not include consumer events. This allows numbers to be accurately compared.

In 2001 and 2002 the fall was dramatic, with 12% fewer visitors in 2001 and 8% fewer in 2002. One caveat is that the previous year, 2000, showed the highest ever number of visitors to exhibitions, so the fall in 2001 was probably from an artificial high. In both 2008 and 2009, visitor numbers fell by 8% and did not start rising again until 2012. We don’t have comparable numbers for 1990-92, but overall numbers for visitors to all exhibitions fell by 14% between 1989 and 1993.

Square metres recover faster than visitor numbers

Square metres are a reasonable proxy for revenues and here we have numbers for all three recessions.

In the recession of 1990-93, the number of square metres sold at UK exhibitions fell by 13.4%. They then recovered quite quickly and were back to 1990 levels by 1997.

Between 2000 and 2003, square metres sold fell by 16.5% and in fact never recovered to their 2000 levels. However, as with visitor numbers, 2000 was the all-time peak of spending on space at UK events and the fall was therefore from a slightly artificial high.

Between 2008 and 2011, sold square metres fell by 16.2% and have never since recovered back to the 2008 level. In 2016, square meters were still 6% below the pre-Lehmann crash.

There is a pattern here. We cannot know whether the period 1990-2022 is typical, nor whether the UK is typical, but these are the numbers we have to work with.

History would therefore suggest that we might lose 20% of ‘expected’ visitors in a recession running from 2022 to 2024.

Sold square metres showed remarkably consistent declines in these recessions – of around 15%. And square metres tend to recover quicker than visitor numbers.

History doesn’t repeat, but it rhymes

A few caveats: History rarely repeats itself, but it does tend to rhyme.

It is important to recognise that this does not mean all shows might lose 20% of their visitors and 15% of their square metres. In the past, larger shows have lost more than smaller shows, though smaller shows disappearing have been part of the picture. And it is certain to be

sector specific.

In the 2000-2002 recession, IT shows lost 38% of their audience, building-related lost 22%, Advertising/Marketing lost 19%, but medical shows increased attendances by 2% and education shows by 5%. The winners and losers by sector are likely to be different this time – we can all make our guesses as to how.

There will be special factors – I am convinced that Crossrail finally opening will have a big effect on ExCeL attendances.

Never make predictions, particularly about the future

At the time of writing, we are far from recovering from the pandemic. Organisers are very coy with their figures – we only tend to hear about shows which are growing. But a fair guess is that we might be moving towards 80% of 2019 (Informa suggested 76% recently). It is obviously impossible to calculate where a recession fits in here.

I prefer never to make predictions, particularly about the future. This is not for every show, but we should not be surprised if by 2024 we are running at 20% below 2019 visitor numbers and 15% below 2019 square metres.

On a positive note to finish. We have weathered recessions and pandemics very successfully in the past, and will do the same with the next one. And the last three recessions have thrown up marvellous opportunities for new and smaller companies to grow fast. The same will happen this time.